[dropcap]W[/dropcap]ith the final authorization received from Consob (the Italian public authority responsible for regulating the Italian financial markets) on Sept. 30th, the Initial Public Offering officially started yesterday with a deadline for completing a successful stock listing by mid-October. The road show aims at reaching a capital increase of around EUR 100 million, as states Lorenzo Langella of BNP Paribas, sponsor bank of the operation, during the presentation held yesterday morning at the Milan office of Boston Consulting Group.

The value of the share capital – before capital increase – has been estimated between 627 and 928 million (min 2,50 € max 3,70 € per share), corrisponding to a capitalization after capital increase between 727 million and 1,076 bln.

The offer, so is explained in an official note, involves a maximum of 87 million shares of Ferretti, equal to 30% of the share capital after capital increase: 40 million shares come from the capital increase and further 47 million from the sale of the shares owned by the shareholders (40 millions of shares of Ferretti International Holding Spa and 7 millions of shares of F Investments Sa).

At the yesterday’s presentation Ferretti Group introduced all the details of the operation to the financial (and nautical) press, illustrating the group’s results, brand positioning, growth objectives and the strategy behind the IPO. At the beginning of his speech, Alberto Galassi, CEO of Ferretti Group, together with Stefano de Vivo (CCO) and Marco Zammarchi (CFO), reminded the audience about the company’s crisis situation of only 5 years ago, comparing it with the diametrically opposite reality of today: a financially strong group with 8 successfull brands well positioned in the market, with the last one, Wally, just entered this year.

Ferretti Group today – The group is present in the market with the widest range of products from 8 meters up until models of 95 meters in lenght (this is the group’s maximum construction capacity), 6 production sites in Italy, production exclusively made in Italy, sales in 70 countries around the world with Italy representing 8% of the turnover. As to financial results, the group’s turnover in 2018 closed at around EUR 609 million, recording an increase of 18.5%, and it is showing even more brilliant results in the first six months of this year .

Alberto Galassi said that today the average sale of Ferretti Group is around EUR 3 million, compared to EUR 2.2 million in 2015 (if we divide the turnover by the number of sales units), which means that the group has worked for a higher positioning, to reach higher average prices and better margins.

The strength of its shareholders – A Chinese giant and an Italian entrepreneur, a winning duo. On one hand, the Chinese Weichai Group, a company with a turnover of EUR 30 billion, which takes second place in the ranking of the best 100 Chinese companies active in the mechanical sector. Weichai, which invested in Ferretti Group in 2012, has several companies listed on Hong Kong as well as a company listed in Frankfurt, has acquired in 2016 the United States-based Dematic, an automation and supply chain optimization company, and has many other investments worldwide. Galassi describes Mr Tan Xuguang, Chairman of Weichai, as “a tiger which sees things where others fail to see anything”, a true visionary man, the only one who saw Ferretti’s potential in 2012 when no Italian wanted to try. The second shareholder is Piero Ferrari (son of Enzo Ferrari and Vice Chairman of Ferrari), who joined the group in 2016 through F Investments. In these two companies, of which Piero Ferrari is a shareholder, Galassi explains, “he puts his name and reputation as well as his constant commitment”. Of Ferrari Spa, Eng. Ferrari has never sold one of his shares and in Ferretti Spa he participates with an active role in the product development, offering a scientific approach, which comes from the automotive. Both shareholders, Weichai and Piero Ferrari, will retain control of the company even after the listing.

Ferretti Group has zero-debt: before listing, Weichai placed in Ferretti Group a shareholder loan of EUR 212 million in 2012. Weichai has been now converted this loan into share capital, effectively giving up and thus canceling out the company’s debt. On the other hand, Ing. Ferrari invested another 15 million euros in the company and another 25 million came from a third Swiss shareholder (Adtech Advanced Technologies, a 3% stake): over the past two months, the company has moved from a net financial position characterized by a shareholders’ loan and by bank debt to a zero-debt position.

The reason behind the IPO – The reason that has moved Ferretti Group was not the desire to raise funds to repay debts. Ferretti, which in 2009 had one billion of debts, today does not need equity to live. They want to enter the stock exchange in order to be able to grow rapidly, and give the group the chance to open up to new services.

The power of brands – Ferretti Group operates with 8 brands (Wally, Ferretti Yachts, Custom Line, Riva, Pershing, Itama, Mochi, CRN) without overlapping. From the most historic, Riva, 170 years of history, one of the oldest shipyards in the world, which with its latest Dolceriva has been a huge success at the recent Cannes Yachting Festival, recording 7 sales in just three weeks at a list price around EUR 1.8 million. Ferretti Yachts is the family boat, “if it was a car, it would be an Audi,” says Galassi. Custom Line, a brand that no longer existed before the rebirth of the group and which was given life with the new ownership: today it represents the growth path of Ferretti Group in the semi custom range from 30 to 50 meters – planing and semi-displacement. And then Wally, “25 years of innovation, technology, use of carbon, genius and insanity, design, performance, such an iconic brand that it is enough to say, I go out with Wally, and everyone knows what it is”, so Galassi talks about Wally. “It’s the formula one of sailing, brought into the group thanks to the intuition of Stefano de Vivo and Marco Zammarchi”. CRN, the jewel of the crown: it is the boat that allows any owner to choose the most appreciated design. Thanks to CRN’s technologies and know-how, Ferretti Group can also develop Riva 50 meters and Pershing 140 (the so-called Ferretti Group Superyacht Division). Pershing, 55 knots of speed. Itama, the most desired Italian classic boat between Rome and Naples. Mochi is the only brand on which the group has not yet put its hands but that, says Galassi, “news will also concern this brand with 50 years of history”.

EBITDA – Ebitda was EUR -22 million in 2014. In 2018 it recorded a positive 53 million, to further improve in 2019: “with Weichai we made an industrial choice, 50 of the EUR 85 millions received in 2014, were promptly reinvested to renew the range. We have created 33 new models, which represented 90% of Ferretti’s turnover in 2018. This means that reinvesting in products gives positive results, and the group will continue to do it”, says Galassi.

The market – In 2014 the global nautical market was worth EUR 14 billion, in 2018 it rose again to EUR 22 billion. It is divided as follows: 2,5 bln are generated with the sail market, 8 bln with outboard, 11,6 bln with inboard. This third segment is the area where Ferretti Group operates, exception made for Wally, which falls within the first two segments (the first Wally brand outboard will be presented in Miami next February). According to forecasts, the segment of the inboard that today represents EUR 11,6 bln is expected to reach 13,4 bln in 2023. Within this segment Ferretti Group represents 8%, with a leadership position.

Market share: this 8% representing Ferretti Group in the inboard segment, is divided into 5 different ranges: the “30-59 feet” range, where Ferretti Group holds 2% of the market, the “60-79 feet” range, where Ferretti Group holds 5%, the “80-99” feet range, where Ferretti records the highest margins starting to show a leading position, and “over 100 feet”, where the group owns a leading position with a market share of 15%. And then the full-custom area, where Ferretti Group is present with CRN (and the Superyacht Division of Ancona): “here the group certainly wants to grow”, as Stefano de Vivo declares, “but in a moderate and balanced way because this is the range that usually generates the lowest marginality”.

Sales strategies – In the last few years Ferretti Group has changed the way they sell their boats, concentrating their strengths on only two channels: below and above 100 feet. For the “under 100 feet” range, the group is organized with 60 dealers in 74 countries around the world: Ferretti Group does not sell to dealers but through dealers, with contracts signed between Ferretti Group and end clients. “This allows the group to directly check incoming and late payments”, says de Vivo. Above 100 feet, boats are already sold to end customers via broker or Ferretti Group directly. A third strategic point regarding sales involves a special team dedicated to the trade-in, i.e. the second-hand market. “Our sales method does not include an agreement to repurchase the boat at x years, this would be a huge risk because the market is uncertain and even the conditions in which the boat will be returned are”, explains de Vivo. “But certainly trade-in is an interesting option, we have the economic strength to support these activities and a part of cash flow can be committed in this direction. The team dedicated to the second-hand market aims to make zero margin, the only margin we want to generate is in the sale of new boats”.

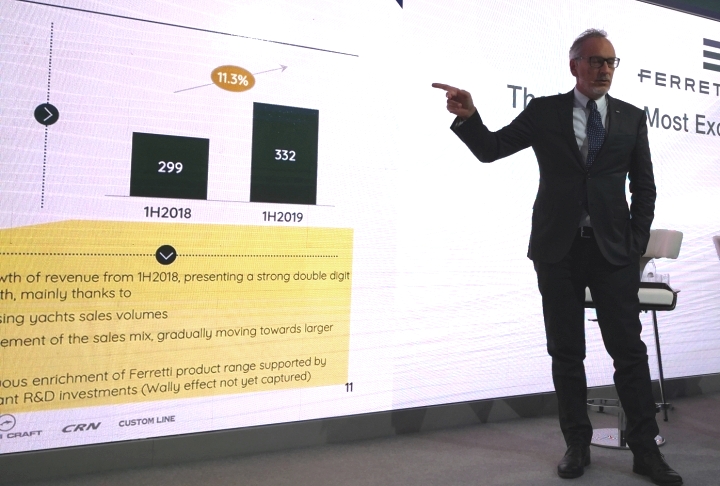

Doubled turnover – Ferretti Group has doubled its turnover from 2014 to 2018, with a growth rate of 18.5%, compared to the average 10% that the rest of the industry has recorded. This was possible thanks to the product innovation, the development of new models and the group’s investment capacity. Ferretti Group has continued to grow also in the first few months of 2019: with a growth rate of 11.3% in the first 6 months of the year, “achieved with the same number of models of 2018, therefore without taking into account the impact given by the Wally brand / product”, points out Zammarchi. The order book for the first six months of 2019 also grew by 19% compared to the first half of 2018 (549 million against 653 million). As for margins, the company grew from EUR -22 million to 53 million in 2018, thanks to production efficiency and design-to-cost model. As Zammarchi explains, “it means that all the models (today 33) before being put on the market are analyzed in terms of positioning and number of units that are assumed to be sold, in terms of price and cost that the group can afford. “If all the parameters are respected, the model is launched. The average gross margin that we have reached today is around 30%, even for those models that initially gave margins only of 10%”.

Drop in profitability in 2017/2018: the reasons. As shown by the data presented yesterday, the Group shows a decrease in margins from 2017 to 2018, from EUR 59 mln to 53 mln. “We opted to facilitate the sale of those models that we still had in the range, models of 2014, but that we had not actually restyled yet; then we sold them devaluing them (devaluation equal to EUR 5 mnl). Second reason: “with the purchase of Wally we have reinforced our production, the after-sales and quality facilities”.

Profitability in 2019: it shows a growth in the first half of this year with a margin of EUR 30 million, an increase of 25.7% compared to the first half of 2018.

Goals of the IPO, five pillars: in terms for production, Ferretti Group will continue with the same semi-serial boats, investing an average of EUR 8/10 mln for each new model up to 50 meters in fiberglass, especially with the Riva and Pershing brand where the company has the highest margin (first pillar). It will develop new Wally products (second pillar) in all possible shapes from 40 feet up, displacing and planing, and will start to penetrate the outboard and sail markets. Then the military sector (third pillar): Ferretti Group successfully entered the military sector with Pershing, a sector in which the group presented to the market a Pershing model literally emptied of any luxury contents and made to all effects a Rina-certified military vessel. “We proposed it to the market and we are selling it well. “Only few shipyards can enter this sector, but there are many other advantages that we can exploit”, expains Galassi. “For us R&D is limited, it is already one of our products, even capital expenditure (CaPex) is small, we can make little investment, it is a boat that we have already developed, the resources are already allocated at the origin of the product development, the time-to-market is fast because the boats are already made and in one year, one year and a half, we can be on the market. Last but not the least, we can offer competitive prices with higher margins”. Currently FSD-Ferretti Security & Defence, Ferretti Group’s division dedicated to Defence and Security, has won a contract for 16 units / patrollers for the Corps of Carabinieri (they chose an hybrid model) and is concluding an important negotiation in the Persian Gulf. “Once this will be signed, our business plan will achieve results much earlier than expected”.

The cyclical nature of the sector is a risk for the market – This is why Galassi sheds light on the riskiness of the sector, which is affected by its cyclical nature. If the first two pillars of Ferretti Group are subject to cyclicality, then from the third pillar onwards the group ensures stability: the defense sector is stable, as are the services and after-sales. With the IPO the group wants in fact to grow in order to introduce also new services: they will develop a new brokerage house, they will launch charter and yacht management services (fourth pillar). To meet this goal, Ferretti Group is looking at the market in order to purchase a new area or an existing yard in the north of the Mediterranean to develop the refitting activities. This fourth pillar will offer the group great marginality with a very low capex, as explains Galassi. Also the fifth pillar is aimed at balancing the cyclical nature of the sector: the brand extension. Lounges all over the world combined with merchandising sales proved to be a great success strategy for Ferretti Group, bringing revenues of one million Euros, with a staff of only two members.

Examples of brand extension include the initiative developed with FIAT for the launch of the Fiat 500 Riva, which brought about 1.5 million Euros to Ferretti. “So with the IPO we do not want to build more, for sure will do it, but the reason of the IPO is to get resources which will allow us to do different things and expand our business into other activities. Our business plan is already fully funded: on one hand, towards our shareholders, we have no debt, on the other hand Ferretti Group can count on a 5-year bank loan of EUR 170 million”.